Pumps, Chips & Pink Slips

March 9, 2026

Market Roundup for the Week

The first week of March 2026 will be remembered as a high-velocity collision between a historic energy crisis, a resilient AI supercycle, and a sudden, sobering crack in the American labor market. While the "Nvidia Standard" and a blockbuster earnings week for the semiconductor sector provided a high-water mark for growth investors, these gains were heavily contested by a dramatic escalation in Middle East tensions and a "Stagflationary" narrative that has fundamentally complicated the Federal Reserve's path forward.

The "Pumps" dominated the early headlines as military strikes on Iranian infrastructure triggered a parabolic move in energy. WTI Crude experienced its largest one-day gain since 2020 on Friday, surging over 12% to settle at $90.90/bbl. With the Strait of Hormuz effectively closed to maritime traffic and Qatar warning of $150 oil, the "tax at the pump" has moved from a lingering concern to an immediate drag on the consumer discretionary (XLY) and industrial (XLI) sectors.

Despite the macro gloom, the "Chips" provided a critical fundamental floor. Broadcom (AVGO) silenced skeptics with a massive earnings beat, forecasting a $100 billion AI chip revenue path by 2027. This was echoed by Marvell Technology (MRVL), which saw its shares skyrocket after hours on Thursday following a raised multi-year outlook. These reports confirmed that while the broader economy may be cooling, the capital expenditure into AI infrastructure remains in a "massive growth" phase, helping the technology sector (XLK) decouple from the Dow's more cyclical struggles.

The most jarring development arrived on Friday morning with the release of the February Non-Farm Payrolls (NFP). The market was hit with a wave of "Pink Slips" as the U.S. unexpectedly lost 92,000 jobs—the worst monthly performance since the height of the pandemic. With the unemployment rate ticking up nearly 4.5% and job gains from previous months being revised downward, the narrative of a "soft landing" has been replaced by fears of an economy teetering on the edge of recession just as inflation (fueled by oil) begins to re-accelerate.

With next week's release of CPI data, the market sits at a precarious junction: record-breaking AI growth is battling a "higher-for-longer" interest rate reality and the most significant geopolitical instability of the decade.

Just over two months into the year, the markets closed 2% BELOW the opening print on Jan 2nd (6878.11).

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

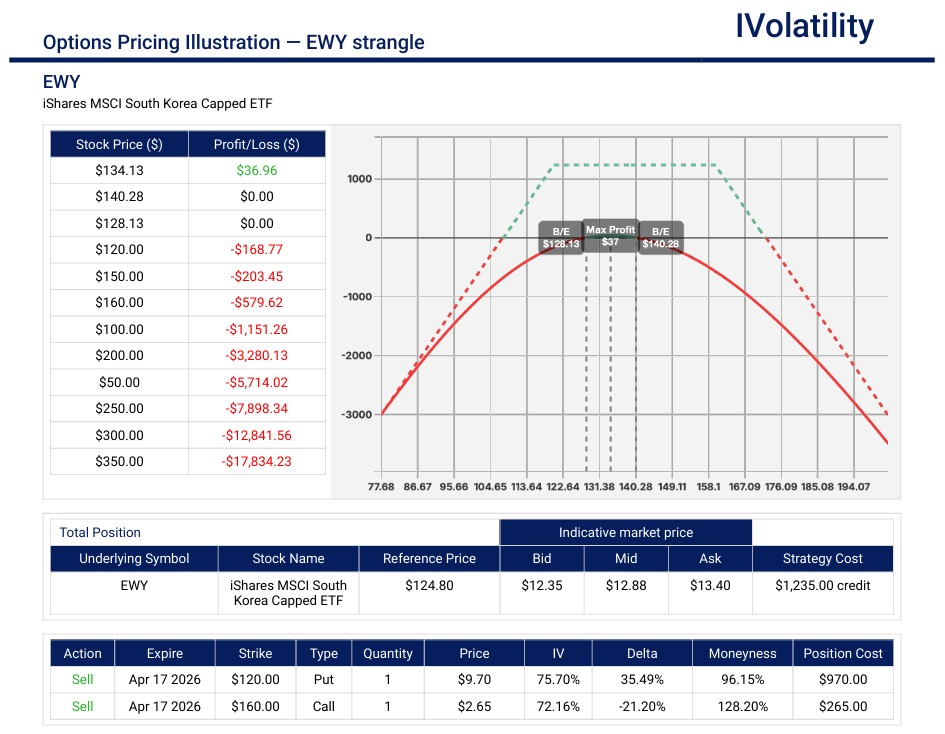

- Underlying: EWY (Ishares South Korea etf, closed at 126.79 on Friday, March 6th)

- Strategy: Sell the April 120/160 strangle

- Rationale: This strangle could be a classic "volatility harvest" play. Given the current market conditions, this trade is essentially a bet on mean reversion after a week of turbulence.

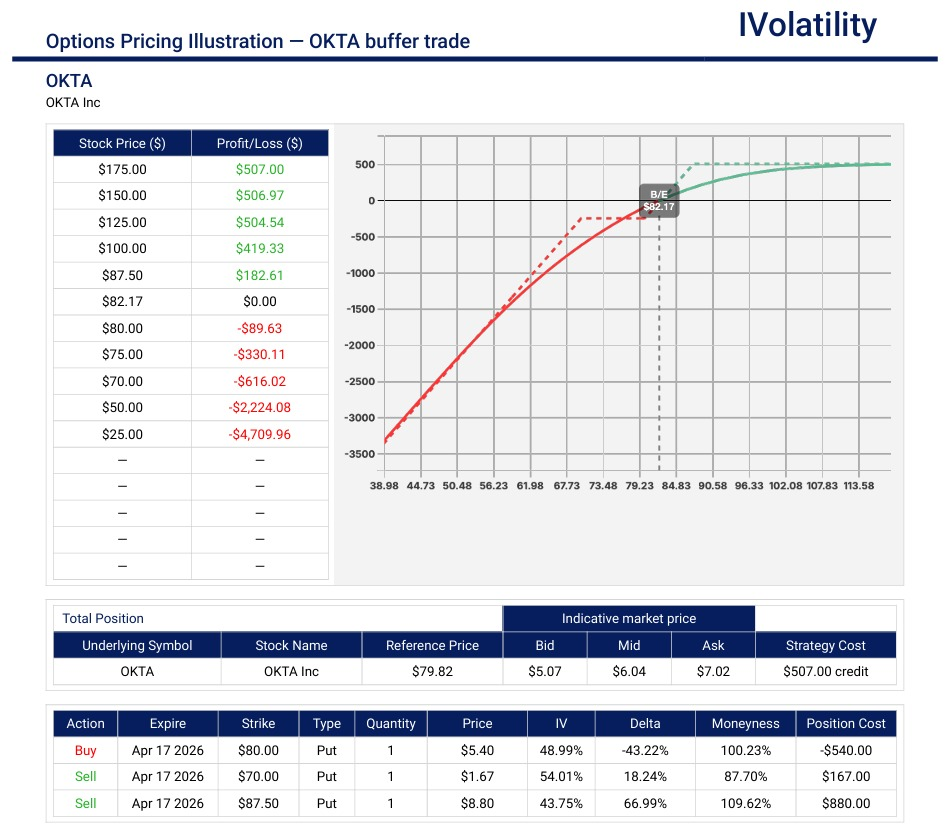

- Underlying: OKTA (closed at 80.68 on Friday, March 6th)

- Strategy: The bullish BUFFER trade

- Set up: Buy the ATM put spread (70/80) and make it as wide as the expected move to the downside; Sell an ITM 87.5put with enough extrinsic value to cover the extrinsic value of the ATM put spread.

- Maximum potential profit = credit received if UL expires above the ITM short put

- Downside breakeven: near the short put of the ATM put spread

Movement of the Major Market Indices:

The week was characterized by a massive divergence in asset classes. While the Russell 2000 (IWM) bore the brunt of the "Stagflation" fear—plummeting over 4% as small caps are most sensitive to rising rates and slowing growth—Crude Oil stole the headlines with a historic 35%+ vertical move.

The VIX surge of nearly 50% reflects a market that was caught off-guard by the intensity of the geopolitical escalation. Notably, Bitcoin acted as a partial hedge or "digital gold" alternative, managing to finish the week in the green despite the broad equity liquidation.

| INDEX | UP | DOWN |

| SPY | -1.98% | |

| QQQ | -1.26% | |

| IWM | -4.02% | |

| DIA | -2.95% | |

| GLD | -2.12% | |

| BTC/USD | 3.42% | |

| TLT | 4.53% | |

| Crude Oil | 35.63% | |

| VIX | 48.56% |

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | -1.20% | |

| FINANCIALS (XL) | -3.10% | |

| INDUSTRIALS (XLI) | -2.70% | |

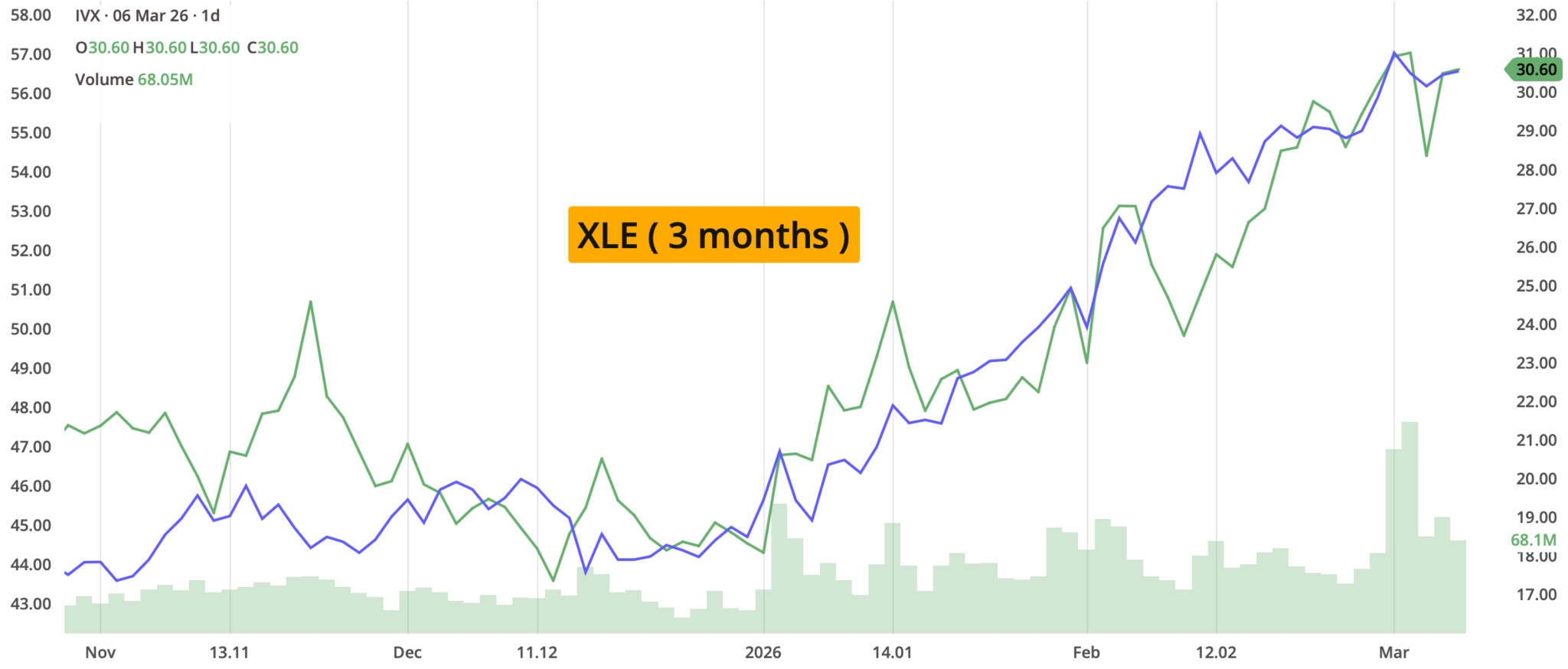

| ENERGY XLE | 14.50% | |

| HEALTHCARE (XLV) | 0.60% | |

| UTILITIES (XLU) | 2.20% | |

| MATERIALS (XLB) | -2.30 | |

| REAL ESTATE (XLRE) | -3.40% | |

| CONSUMER STAPLES (XLP) | 1.50% | |

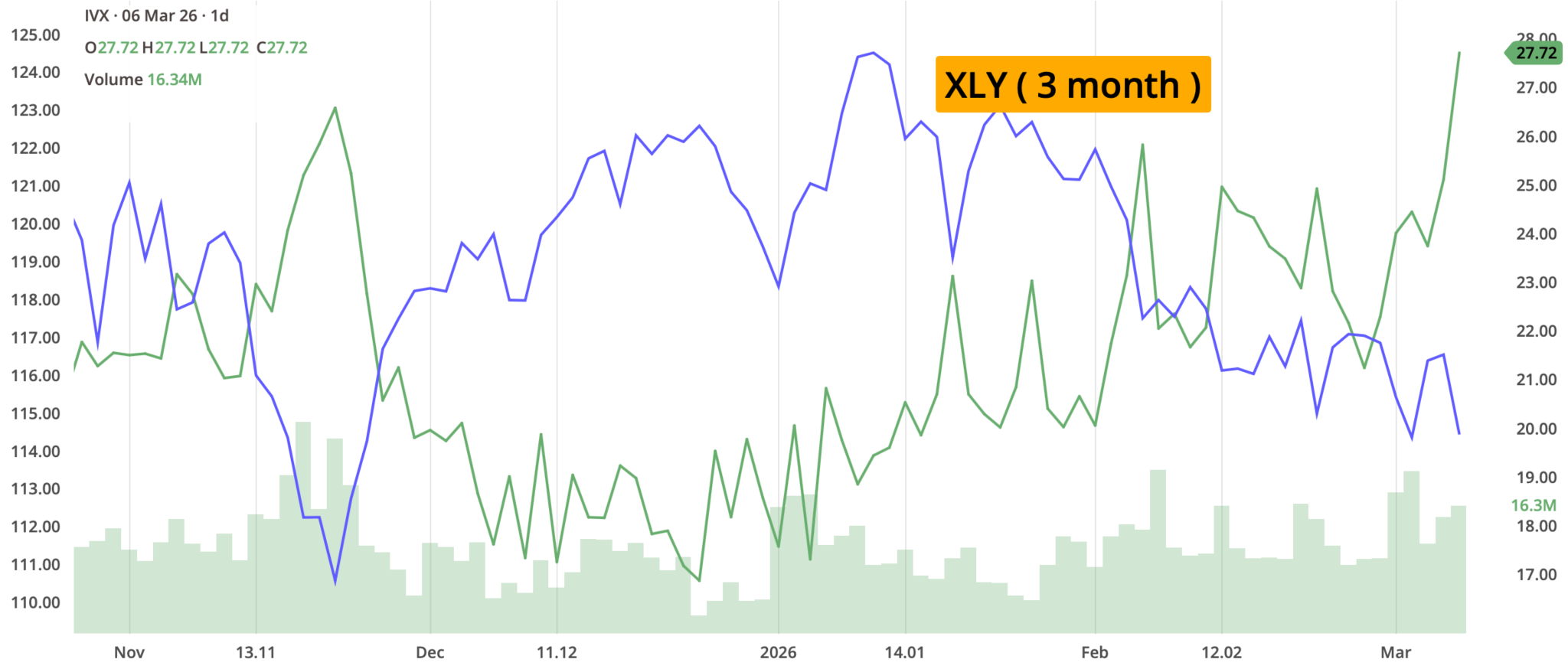

| CONSUMER DISCRETIONARY (XLY) | -4.00% |

The undisputed winner of the week was XLE, with WTI Crude jumping over 35%.

As growth projections for the first half of 2026 were slashed following the weak Jobs report, investors moved into defensive sectors like XLU, XLP and XLV. Despite the Broadcom bounce, the XLK sector finished down 1.2% as rising yields and global supply chain concerns from the Middle East conflict weighed on valuations. The week's laggard, XLY, fell as fears of higher gasoline prices and a slowing labor market dampened outlooks.

Notable gainers for the week of March 2nd–6th:

In a week marred by a historic energy spike and the "Stagflation" shock of Friday's labor data, the standout winners were primarily those insulated by M&A activity or those demonstrating undeniable momentum in the AI infrastructure supercycle.

- Day One Biopharmaceuticals (DAWN) was the week's top performer, skyrocketing over 65% on Friday alone. The surge followed the announcement that French pharma giant Servier will acquire the company in an all-cash deal. The acquisition focuses on Day One's lead pediatric oncology asset, OJEMDA, which has seen 172% year-over-year revenue growth.

- Marvell Technology (MRVL): Gained 18.35% for the week, with a massive breakout on Friday. Despite the broader market sell-off, Marvell reported a Q4 "Data Center" beat, with revenue jumping 42% year-over-year. Management's guidance was the real catalyst, as they now project fiscal 2028 revenue to reach $15 billion driven by AI networking and custom silicon demand.

- Samsara (IOT): Rose over 19% this week. The "Internet of Things" leader surpassed Q4 estimates with a 28% jump in revenue to $444.3M. Investors cheered the company's fiscal 2027 guidance, which suggests that even in a slowing economy, the demand for enterprise fleet and asset digitisation remains a priority for industrial efficiency.

- Sable Offshore Corp. (SOC): Climbed significantly, emerging as a top monthly gainer with a 67% advance in March. As the week's energy crisis unfolded, Sable became a primary beneficiary of the hunt for domestic offshore production assets as Middle East supply lines faced unprecedented risk.

- Broadcom (AVGO) finished the week up nearly 5%, effectively "saving" the Nasdaq from a deeper slide. CEO Hock Tan's commentary regarding a $100 billion AI chip revenue path by 2027 and the addition of OpenAI as its sixth custom chip customer provided a critical fundamental floor for the semiconductor sector.

Notable losers for the week of February 2nd–6th:

The week's "Stagflation" narrative and the geopolitical energy shock left nowhere to hide for sectors sensitive to fuel costs, consumer spending, or interest rate fluctuations. The laggards of the week represented a market that is aggressively pricing in a slowdown in domestic growth.

- Sunrun (RUN) dropped 35% for the week. The residential solar leader was decimated as a "double whammy" hit the sector: a weak 2026 outlook following an analyst downgrade, followed by Friday's yield spike which could increase the cost of capital for solar installations.

- Molina Healthcare (MOH) continued its downward spiral, losing another 15% this week. The stock is still reeling from the disastrous Medicaid outlook flagged in late February. The "Red Friday" jobs report added fuel to the fire, as fears of a contracting labor market suggest a potential drop in employer-sponsored enrollment and further margin compression.

- Gap (GAP) plunged over 8% following its Q4 earnings report. While the company is attempting a brand turnaround, missing earnings estimates and citing "extreme weather" store closures in January failed to inspire confidence. In a week where the consumer is facing a "tax at the pump" from rising oil, apparel retailers were among the first to be liquidated.

- Old Dominion Freight Line (ODFL) sank nearly 8% this week. As a bellwether for the domestic economy, Old Dominion's slide reflects a "Perfect Storm" for the trucking industry: skyrocketing diesel prices (up 35% with Crude) combined with a shockingly weak Non-Farm Payrolls report signaling a slowdown in freight volumes.

- Southwest Airlines (LUV) fell nearly 7% for the week. The airline sector was the primary casualty of the Middle East escalation. With WTI Crude hitting $90/bbl, jet fuel costs are expected to erode 2026 profit margins entirely for carriers unable to pass on costs to a weakening consumer.

- Unity Software (U) lost an additional 12% this week. The market skepticism regarding its growth forecast persists, especially as "Agentic AI" tools continue to threaten its core business model.

Review selected market indices below:

Daily Notable Market Action

The first week of March was defined by a shift from the "Nvidia Primary" to a full-blown "Geopolitical Pivot." As military tensions escalated in the Middle East, the market's internal mechanics favored Energy and Defense, while the "Agentic AI" narrative continued to disrupt legacy software and hardware valuations.

Monday's Markets and News:

The market opened to a "Gap Down" as traders reacted to weekend reports of coordinated U.S.-Israeli strikes on Iranian strategic facilities. Brent crude spiked as much as 13% overnight on fears of a Strait of Hormuz closure before settling lower. Equities swung from deep early losses to a mixed close. The Dow fell 0.1%, while the Nasdaq managed a 0.4% gain as investors viewed the conflict as a potential catalyst for increased defense and energy spending.

Monday's Movers to the Upside:

- Northrop Grumman (NOC) gained 6% on expectations of sustained high military expenditures.

- Nvidia (NVDA) added 3% as the "buy the dip" mentality remained strongest in the AI chip leader.

Monday's Movers to the Downside:

- United Airlines (UAL) fell sharply (along with the airline sector) as Crude Oil's spike signaled a massive hit to forward fuel margins.

- Salesforce (CRM) dropped nearly 2.5% as the rotation out of high-multiple software continued.

Tuesday's Markets and News:

Sentiment soured as the conflict entered its fourth day with reports of Iranian missile retaliation near U.S. interests in the Gulf. The S&P 500 closed below its 100-day moving average for the first time in over three months. A broad-based "Risk-Off" selloff took hold. Treasury yields climbed for a second session, with the 10-year touching 4.11%, reflecting fears that surging oil prices will force the Fed to stay "Hawkish".

Tuesday's Movers to the Upside:

- AeroVironment (AVAV) surged nearly 8.5% as demand for tactical drone systems became a primary focus of the regional conflict.

- Energy Select Sector (XLE) advanced 2% as WTI Crude settled up over 6% at $71.23/bbl.

Tuesday's Movers to the Downside:

- Intel (INTC) plunged over 5% as concerns over global supply chain disruptions outweighed AI optimism.

- Caterpillar (CAT) dropped 4% as the "Plan B" tariff trajectory and rising input costs dampened the industrial outlook.

Wednesday's Markets and News:

A classic "relief rally" took shape as oil prices paused their vertical ascent and domestic economic data suggested the U.S. consumer remains resilient despite the global chaos. The S&P 500 rose 0.8%, clawing back most of the "War losses". Strength was driven by the ADP Employment Report and a cooling in the Brent Crude spike, which settled back toward $81/bbl.

Wednesday's Movers to the Upside:

- Olaplex (OLPX) skyrocketed 19% in aggressive positioning ahead of its Q4 earnings report.

- Ross Stores (ROST) climbed 8% after reporting a revenue beat and citing "solid momentum" heading into 2026.

Wednesday's Movers to the Downside:

- Albany International (AIN) fell nearly 4.5% following a mixed reception to its EPS performance and news of institutional selling.

- Cummins (CMI) declined over 3% as short interest increased amid concerns over a softening medium-duty truck market in China.

Thursday's Markets and News:

The technology sector decoupled from the broader macro gloom following a massive earnings beat from the AI giant, AVGO. AVGO results acted as a floor for the Nasdaq, though the Dow remained under pressure from a rotation out of value-retailing after a high-profile downgrade of Walmart.

Thursday's Movers to the Upside:

- Broadcom (AVGO) gained over 5% in after-hours and early trading after projecting $100 billion in AI chip sales by next year.

- Paramount (PARA) jumped on renewed takeover drama as Netflix officially bowed out of the bidding war for Warner Bros assets.

Thursday's Movers to the Downside:

- Corning (GLW) plunged nearly 9% following an analyst report highlighting valuation concerns and recent insider selling.

- Walmart (WMT) dropped nearly 4% after an analyst downgraded the stock to "Hold," citing an overextended P/E ratio relative to peers.

Friday's Markets and News:

The markets experienced a "Double Whammy" of dismal labor data and a parabolic move in energy prices sparking fears of a stagflationary spiral. The February Jobs Report arrived far weaker than even the most pessimistic forecasts, while the rhetoric surrounding the Middle East conflict reached a fever pitch.

Equities plunged from the opening bell. The Dow Jones plummeted as many as 945 points before settling with a loss of 453. The S&P 500 fell 1.3%, and the Nasdaq dropped 1.6%. The Bureau of Labor Statistics reported a shocking loss of 92,000 jobs in February (vs. 60,000 expected gain), while the unemployment rate ticked up to 4.4%.

WTI Crude prices surged a staggering 12.2% to flirt with $90.90/bbl following President Trump's "unconditional surrender" demand toward Iran and reports that maritime traffic through the Strait of Hormuz has effectively halted.

Friday's Movers to the Upside:

- Day One Biopharmaceuticals (DAWN) skyrocketed 66% following a $2.5 billion cash acquisition deal by the Servier Group.

- Marvell Technology (MRVL) popped over 11% after beating earnings expectations and issuing a robust fiscal 2028 revenue outlook of $15 billion.

- Samsara (IOT) jumped 11% on the back of an earnings beat for the fleet management software provider.

Friday's Movers to the Downside:

- Old Dominion Freight Line (ODFL) sank nearly 8% as surging diesel prices and the weak jobs report signaled a sharp slowdown in trucking demand.

- Gap (GAP) plunged over 8% after missing Q4 earnings estimates, citing store closures from January's extreme weather.

- Southwest Airlines (LUV) fell nearly 7% as the combination of a labor slowdown and skyrocketing jet fuel costs hammered the airline sector.

Notable Earnings to be announced March 9th–13th:

With the "Nvidia Hangover" behind us and energy prices reaching record highs, the market's focus shifts toward the resilience of enterprise cloud spending and the potential "wealth-building" announcement surrounding the SpaceX IPO. This week is a critical test for legacy hardware and high-growth AI software, providing the first corporate reactions to the historic surge in crude oil and the sudden cooling of the labor market.

The actual date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday: HPE / CASY / FCEL

Tuesday: ORCL / KOHL / NIO

Wednesday: PATH

Thursday: ADBE / RBRK / S / SKIN

Friday: No major market-moving earnings reports have been confirmed

According to earningswhisper.com, the expectations are :

Beat: ORCL / ADBE / PATH / RBRK / CASY / FCEL

Miss: HPE / KSS / NIO

Inline: S

Earnings "Watch Items":

- The Enterprise Cloud Barometer (ORCL, ADBE): Following Alphabet's recent acknowledgment of AI infrastructure risks, investors will look to Oracle and Adobe for confirmation that AI-driven demand is translating into accelerated revenue growth rather than just rising capital expenditures.

- The Hardware Handover (HPE): Hewlett Packard Enterprise will provide a vital data point on whether the AI server demand seen in Broadcom's recent print is consistent across the broader enterprise hardware ecosystem.

- AI Software Disruption (PATH, RBRK, S): After the "Claude Code" release earlier this season, these reports will be scrutinized for signs of AI-driven displacement in legacy automation and cybersecurity business models.

- Consumer Health (KSS, CASY, SKIN): As wholesale inflation pressures mount, these results will indicate how much of the "Tax at the pump" from surging oil prices is being absorbed by retail and convenience store margins.

Economic Calendar for Week of March 9th–13th:

Following the "Labor Shock" on March 6th, which saw an unexpected loss of 92,000 jobs, the coming week shifts focus to Inflation and GDP Resilience. The market is desperately looking for data to justify a "Fed Pivot," but with oil prices flirting with $90/bbl, the risk of stagflation looms large. This week's CPI and Core PCE prints will be the ultimate arbiters of whether the Fed can afford to cut rates in March or if they must remain "Hawkish" to combat energy-driven price spikes.

The daily schedule of notable economic data releases is:

Monday: NY Fed 1-Yr Inflation Expectations

Consumer Sentiment: A key look at whether Americans expect current energy spikes to be transitory or structural.

Tuesday: NFIB Business Optimism Index

Small Business Health: Following the weak payrolls, investors want to see if small business hiring intentions are actually collapsing.

Wednesday: Consumer Price Index (CPI) YoY

The Main Event: The market is banking on a sub-3% print. Any "hot" surprise here would likely eliminate hope for a March rate cut.

Thursday: Producer Price Index (PPI) YoY

Wholesale Inflation: Measures the "input cost" pressure on corporations. A rise here signals further margin squeeze for retailers.

Friday: GDP (Second Estimate) Q4 2025

Growth Check: A revision downward would heighten recession fears, while an upward revision would suggest the economy is overheated.

Friday: Core PCE Price Index (Jan)

Fed's Preferred Gauge: Released alongside personal income data; this is the final "Inflation Anchor" the Fed weighs before its meetings.

The Federal Reserve is now trapped between a weakening labor market and accelerating energy costs. The loss of 92k jobs and a 4.4% unemployment rate suggest the "restrictive" policy is finally breaking the back of the labor market and could be viewed as a case for further dropping of interest rates. If Wednesday's CPI or Friday's PCE shows inflation "sticky" above 2.5%, the Fed might hesitate to cut rates without risking a 1970s-style inflationary rebound fueled by the current Middle East oil shock.

Closing Thoughts

The Rise of "Orbital Compute" and the Final Frontier of AI Infrastructure

While the market spent the week obsessing over Middle East oil spikes and the Nvidia "hangover", a far more permanent shift is quietly orbiting 300 miles above earth. In 2026, we are witnessing the birth of Orbital Compute—the integration of high-performance AI data centers directly into satellite constellations.

For decades, space was a "bandwidth" game—getting data from Point A to Point B. But as terrestrial power grids in places like Virginia and Ireland buckle under the 50-gigawatt demand of AI models, the "SpaceX adjacency" stocks are beginning to price in a new reality: Space is the ultimate heat sink.

With the rumored SpaceX IPO targeting mid-2026 at a valuation exceeding $1 trillion, the market is searching for a "Space-AI" anchor. We are moving away from "speculative" space stocks and toward "infrastructure" plays—companies providing radiation-tolerant electronics, optical laser comms, and in-orbit thermal management.

Orbital compute isn't just about power; it's about bypass. AI agents running on orbital hardware can operate outside the latency and regulatory "walls" of terrestrial fiber networks. By year-end, we expect the first "Sovereign AI" satellite launches, where nations host their primary LLMs in orbit to ensure data continuity regardless of terrestrial geopolitical conflict.

Just as oil defined the 20th century, "Tokens per Watt" will define the 21st. If compute can be successfully offshored to orbit, the traditional "Utility" sector (XLU) may face a long-term disruption as AI capex migrates from the local grid to the stars.

We often look at the stars and think of exploration, but capital markets are starting to look at the stars and see Real Estate. In a world where terrestrial data center permits take 5 years to clear, the 2026 investor might ask: Who owns the "land" in Low Earth Orbit, and who provides the power to the agents living there?

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.