"Plan B" & the NVDA Test

March 2, 2026

Market Roundup for the Week

The week was defined by a delicate tug-of-war between stellar corporate earnings and a complex, shifting landscape of trade policy and inflation data. While the market opened the week celebrating the constitutional check on executive power, sentiment quickly shifted as the structural reality of "Plan B" trade litigation took hold.

Following the Supreme Court's 6-3 ruling on February 20th—which struck down the broad "Liberation Day" tariffs as an unconstitutional expansion of the International Emergency Economic Powers Act (IEEPA)—the administration moved with unexpected speed. By Tuesday morning, the White House signaled a pivot toward alternative legal authorities, specifically Section 122 (balance-of-payments) and Section 232 (national security) of the Trade Act. This "Plan B" strategy suggests a transition from blanket country-level duties to more surgical, industry-specific tariff floors, likely centered around a 15% baseline. The immediate result was a spike in volatility as businesses realized that while the legal framework had changed, the protectionist trajectory remained intact.

The week's undisputed centerpiece was NVDA Q4 earnings report on Wednesday. Silencing skeptics, the chip giant reported record revenue of $68.1 billion (up 73% year-over-year) and an EPS of $1.62. This "Nvidia Standard" provided a temporary floor for the Nasdaq, confirming that the AI infrastructure supercycle is still in its expansionary phase. However, this corporate strength met significant macro friction on Friday. The Producer Price Index (PPI) arrived hotter than expected at 2.9%, driven by wholesalers passing on residual tariff costs. This was followed by the Core PCE print, which—though cooling slightly to 2.74%—reinforced the Federal Reserve's "Hawkish Pause" narrative.

Beneath the headline indices, two undercurrents added to the week's "50,000pt Hangover". Geopolitical tensions intensified as the 10-day window for a diplomatic accord with Iran neared its expiration, pushing Crude Oil (WTI) toward $67/bbl. Simultaneously, the private credit "liquidity scare" flagged last week continued to percolate; shares of alternative asset managers remained under pressure as investors scrutinized the transparency of shadow banking portfolios.

The week concluded with a classic "defensive rotation," as capital flowed out of the Dow's cyclical components and into Utilities (XLU) and Consumer Staples (XLP), reflecting a market that is fundamentally "Risk-Off" despite the AI-driven headlines.

Two months into the year, the markets closed at literally the same level (6878.90) as the opening print on Jan 2nd (6878.11).

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

With the VIX retreating despite the previous Friday sell-off, premium sellers are finding opportunities in name-brand retail and defensive tech.

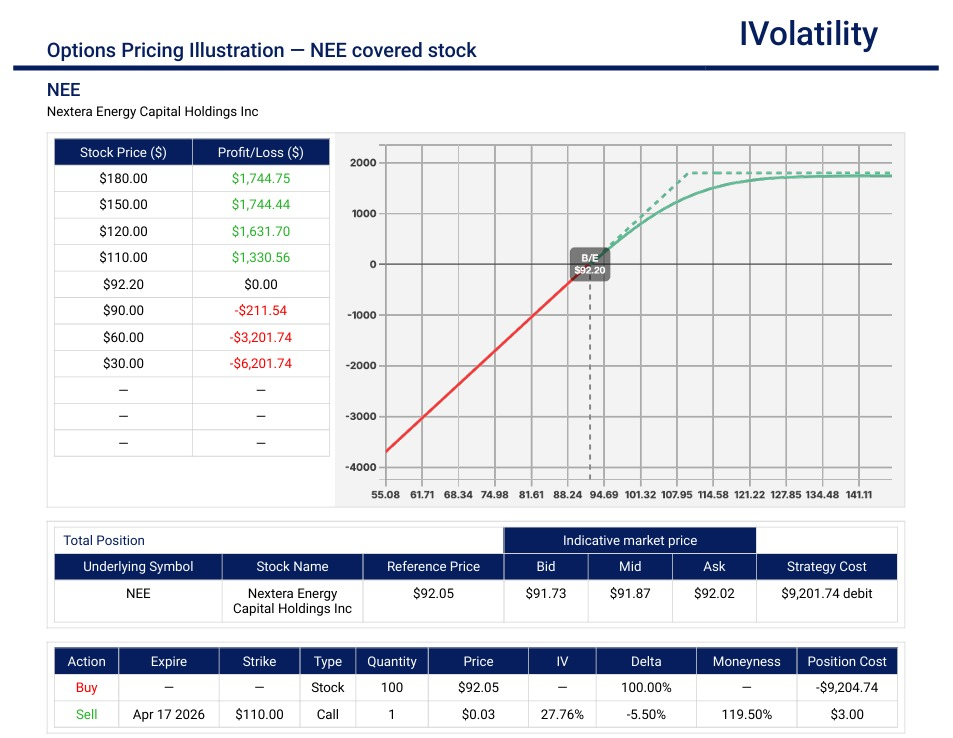

- NEE (Closed at 93.75 on Friday, February 27th)

This underlying could serve as a prime candidate for Covered Calls as the "Yield-Starved" capital moves back into Utilities.

- Strategy: bullish covered stock

- Trade: buy 100 shares of stock and sell the Apr17 100call against it

- Cost basis: around $9250

- Max potential profit: $750 if NEE expires above 100 by April 17th

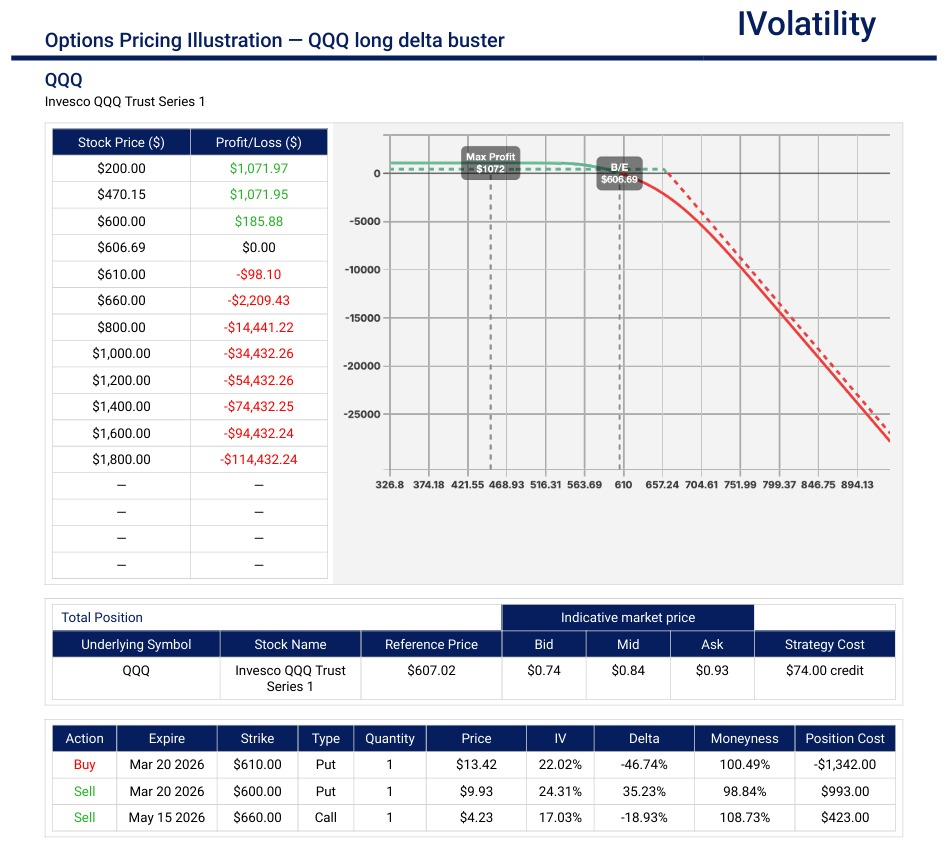

PnL Calculator from the IVolLive Web - QQQ (Closed at $607.47 on Friday, February 27th)

With the tech sector depressed and no good news in sight, a trader could try to capture further downside moves.

- Strategy: Long Delta Buster

- Trade: Buy the Mar20 600/610 long put spread and finance the purchase with the sale of a May15 660call

- Net Credit: about 45c

- Max potential profit: $1000 if QQQ expires below 600 by Mar20

PnL Calculator from the IVolLive Web

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

| SPY | -0.84% | |

| QQQ | -0.41% | |

| IWM | -0.93% | |

| DIA | -1.57% | |

| GLD | 1.28% | |

| BTC/USD | -3.15% | |

| TLT | -2.94% | |

| Crude Oil | 1.07% | |

| VIX | -3.35% |

The Yield Drop: The move from 4.08% to 3.96% is the most significant macro shift this week, triggered by the cooling Core PCE data on Friday morning.

Dow Underperformance: The -1.57% drop in the DIA reflects the "50,000pt Hangover" as industrial and value names faced pressure from the "Plan B" tariff uncertainty.

VIX Divergence: Even though the indices were mostly down, the VIX actually fell 3.35%, suggesting that the market isn't "panicking"—it's simply repricing.

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | -1.60% | |

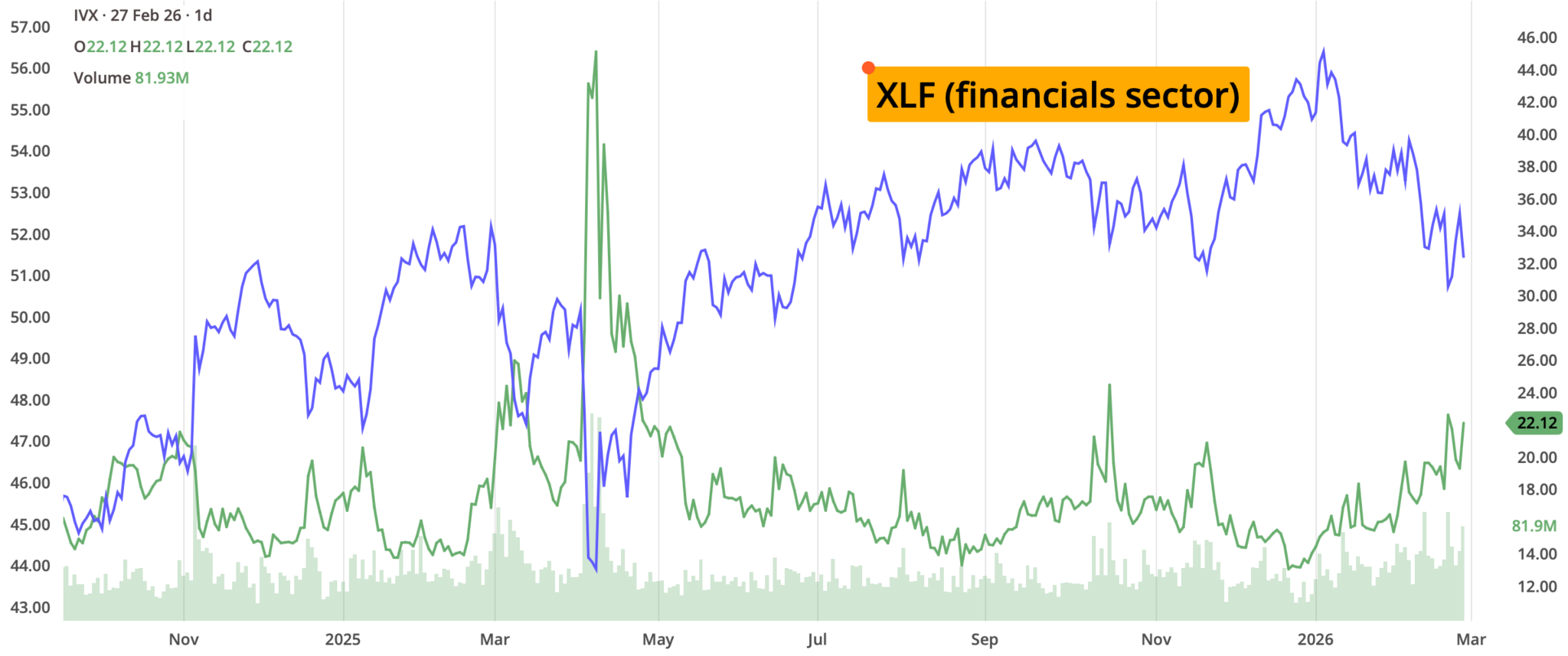

| FINANCIALS (XL) | -2.04% | |

| INDUSTRIALS (XLI) | -0.95% | |

| ENERGY XLE | 1.15% | |

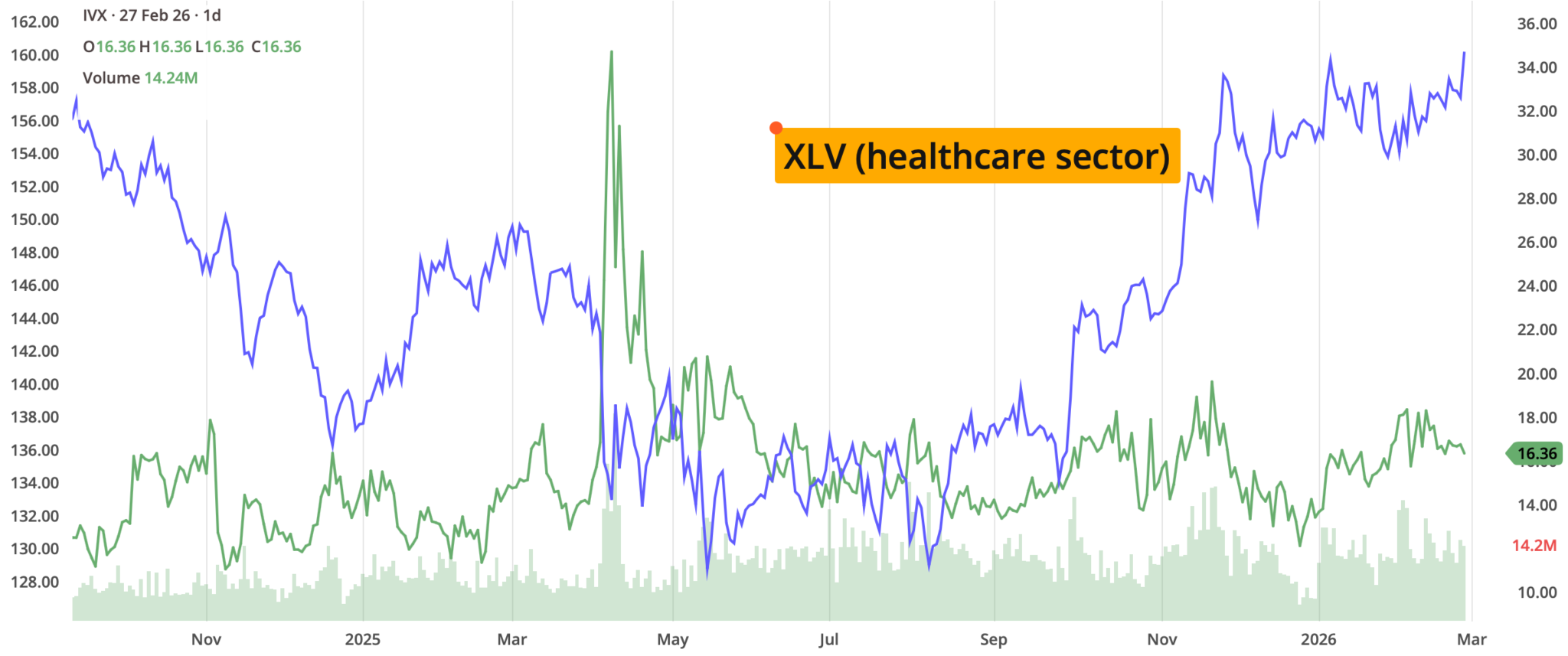

| HEALTHCARE (XLV) | 1.77% | |

| UTILITIES (XLU) | 1.40% | |

| MATERIALS (XLB) | 0.77% | |

| REAL ESTATE (XLRE) | 0.48% | |

| CONSUMER STAPLES (XLP) | 1.29% | |

| CONSUMER DISCRETIONARY (XLY) | -1.16% |

The Laggard: Financials (XLF) were the worst performers at -2.04%, as the market began pricing in higher risk for regional banks exposed to "shadow banking" loans.

The Winner: Healthcare (XLV) took the top spot (+1.77%), largely due to a rotation into value-based pharma as investors locked in Tech profits.

The Tech Paradox: Despite Nvidia's record week, the XLK actually fell 1.60% for the week, highlighting that the "AI halo" wasn't enough to lift the entire sector.

Notable gainers for the week of February 23rd–27th:

Despite a choppy tape and the Dow's 500-point slide, specific pockets of the market found significant momentum. The week's winners were defined by two themes: those who silenced the skeptics with undeniable growth (Nvidia) and those who provided a safe haven as the 10-year yield retreated below the 4.00% mark.

Walmart (WMT) surged over 4% and the gain was fueled by a Q4 earnings transcript that highlighted a 24% jump in e-commerce and 10.5% growth in adjusted operating income, making it a primary destination for defensive capital.

Dominion Energy (D) climbed nearly 3%. The drop in the 10-year yield from 4.08% to 3.96% acted as a springboard for utilities and investors locked in yields that now look increasingly attractive compared to volatile treasury notes.

First Majestic Silver (AG) rose 4.35% As a "double play" on industrial demand and a hedge against the Friday "Sell the News" event, silver miners outpaced the broader market. AG climbed as Gold and Silver prices caught a bid on the weak PCE-induced dollar dip.

Notable losers for the week of February 23rd–27th:

The euphoria of Dow 50,000 was replaced by a ruthless "flight to quality," leaving speculative high-growth and illiquid financial plays in the lurch. This week's laggards reveal a market that is aggressively punishing any perceived weakness in liquidity or susceptibility to AI-driven disruption.

Molina Healthcare (MOH) dropped nearly 24% and was the week's undisputed casualty. Following a disastrous Medicaid outlook, the stock seemed to fail to find a floor. The collapse may reflect deep-seated fears regarding reimbursement rates and margin compression in the government-sponsored healthcare space.

Unity Software (U) lost over 18%, continuing its "Software Slump" spiral. The market remains skeptical of the company's growth forecast in an era where generative AI tools are rapidly lowering the barriers to 3D asset creation, potentially commoditizing Unity's core engine.

Blue Owl Capital (OWL) dropped over 8%. The "Shadow Banking" scare took a bite out of Blue Owl and the restriction on redemptions in its retail-focused credit fund sparked a broader reassessment of liquidity in private markets, leading to a steady exit by institutional holders throughout the week.

Peloton (PTON) lost over 12%. Despite efforts to rebrand, the missed revenue targets from the holiday quarter and a lack of clear catalysts caused a steady bleed in the share price as investors rotated into "Safe Haven" retailers like Walmart.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

The market opened to a "Tariff Reset" as President Trump signed an executive order imposing a 15% global tariff under Section 122 of the 1974 Trade Act, bypassing the SCOTUS ruling against IEEPA. This "Plan B" sparked immediate volatility, sending the Dow down over 800 points as trade-sensitive sectors recoiled.

The Trump administration boosted remaining tariffs from 10% to 15% over the weekend under the authority of Section 122 of the Trade Act of 1974. That part's important: Section 122 only lets the President impose levies for 150 days, and Congress would have to approve extending it after that—setting us up for a new tariff showdown this summer.

Equities sank as investors struggled to digest the effects of new tariffs, particularly after President Trump threatened even higher levies against countries that "play games" with ongoing trade agreements.

Tariff jitters were great news for gold and silver, while bitcoin tumbled below $64,000 at one point today.

Of further interest:

- Democrats introduced legislation to return the $175 billion in refunds the government owes to importers after the Supreme Court's ruling last week.

- EU lawmakers postponed voting on the bloc's previous tariff deal with the US after Trump's new "global" tariffs were announced.

- Strategy isn't letting the crypto bloodbath slow down its bitcoin buying.

- Goldman Sachs says AI investments contributed "basically zero" to US economic growth last year.

- Meanwhile, activist investors are circling Blue Owl like vultures.

Monday's Movers to the Upside:

- Domino's Pizza jumped over 4% on strong comparable-sales growth and continued restaurant expansion.

- Arcellx surged nearly 80% after Gilead Sciences agreed to acquire the biotech company for $7.8 billion, an 80% premium to its prior close.

- PayPal gained nearly 6% on reports of takeover interest, with at least one large rival eyeing the full company and others circling select assets.

- ImmunityBio climbed nearly 13% after posting 700% year over year revenue growth and outlining expanded lung cancer approvals alongside global commercialization plans.

- Veris Residential jumped over 12% after agreeing to be acquired by a consortium led by Affinius Capital.

Monday's Movers to the Downside:

- IBM plunged over 13% after Anthropic revealed that Claude Code could automate the use of a key programming language.

- Cybersecurity names kept dropping following Anthropic's introduction of new AI security capabilities. CrowdStrike lost nearly 10%, Zscaler fell over 10%, and Okta dropped nearly 6.5%.

- Docusign slid over 6%, hitting a 52-week low as broader concerns about growth prospects and softer tech sector conditions, along with a downgrade from Jefferies, weighed on shares.

- DoorDash dipped nearly 7% as the company extended its delivery pause in New York City amid a major snowstorm.

- Financial stocks weakened overall, with KKR down nearly 9%, Blackstone off over 6%, Blue Owl sliding over 3%, and American Express retreating over 7% as private credit stress rippled through markets.

Tuesday's Markets and News:

Tariff confusion reigned once again as the US put 10% tariffs on all goods not covered by previous exemptions, rather than the 15% that President Trump promised to impose "effective immediately" over the weekend.

Investors took this as a sign that the "TACO trade" was back in full effect, so they did what they do best: bought the dip in tech stocks, and pushed all three major indexes higher.

The risk-on attitude pulled gold and silver down a bit, while oil also fell, as traders reconsidered the likelihood of a US attack on Iran after the Pentagon urged caution.

Market participants pivoted focus toward the President's State of the Union (SOTU) address and Wednesday's Nvidia print. A rotation into "HALO" stocks (Heavy Assets, Low Obsolescence) supported the Dow, while biotech saw explosive moves on positive trial data.

Of further interest:

- Spirit Airlines struck a deal with its lenders to help the airline fly out of bankruptcy.

- A new study from Harvard found that AI can predict 71% of active managers' trades.

- FedEx is suing the Trump administration to get refunds from the tariffs the Supreme Court just deemed illegal.

- Financial stocks are having their worst start to the year in a decade.

- Famed activist investor Boaz Weinstein warned that the private credit industry is in the "super-early innings of the wheels coming off the car".

- Microsoft announced a partnership with SpaceX's Starlink to expand internet service globally.

Tuesday's Movers to the Upside:

- Investors recalibrated software valuations amid renewed attention around Anthropic's Claude Code tool. CRM jumped 4%, DOCU popped over 2.5%, LZ climbed over 2.5%, IBM rebounded nearly 3%, and FDS gained nearly 6%.

- HD rose nearly 2% as earnings beat expectations for the first time in a year, even as overall sales declined.

- VIR climbed nearly 30% on promising Phase 1 results for its prostate cancer drug.

- KEYS gained 23% following a major earnings beat, fueled by surging infrastructure and AI-related demand.

- UCTT added over 17% with fourth-quarter revenue topping estimates, signaling continued strength in semiconductor equipment supply chains.

Tuesday's Movers to the Downside:

- Novo Nordisk slid nearly 3% after announcing plans to cut monthly list prices for Wegovy and Ozempic by up to 50% starting in 2027.

- Dillard's fell nearly 8% as weaker-than-expected holiday revenue, partly blamed on winter storms impacting over a third of its stores, weighed on results.

- Planet Fitness dropped nearly 9% as soft forward guidance overshadowed an otherwise solid fourth quarter.

- Expeditors International declined over 7% despite a narrow earnings beat, with operating income missing expectations.

- Whirlpool lost nearly 14% following the announcement of public stock and depositary share offerings aimed at reducing debt and funding automation investments.

Wednesday's Markets and News:

Investors who have spent the last few days rotating out of tech rotated right back in today, even as the HALO trade takes over Wall Street. Gold, silver, and copper all climbed today as investors searched for stability, but the biggest winner of the day was platinum.

Bitcoin rebounded, snapping a three-day losing streak.

All eyes were on the "Nvidia Primary." All eyes now turned to Nvidia's earnings this evening, with the chipmaker's report seen as a key test for the AI trade. Markets trended higher through the session on tech strength.

Wednesday's Movers to the Upside:

- Oracle rose over 1% as Oppenheimer upgraded the stock to Buy, arguing the recent selloff has improved the risk-reward profile.

- Coinbase gained 13.5% on news it will roll out 0% commission trading for US stocks and ETFs.

- Netflix added nearly 6% amid expectations that it will pull back its bid for Warner Bros. Discovery.

- Identity platform operator Clear Secure climbed nearly 40% following stronger-than-expected fourth-quarter revenue and profit.

- Safety technology company Axon Enterprise jumped 17.5% as fourth-quarter results topped estimates, fueled by growing adoption of its AI-enabled software tools.

- Cava Group advanced 26% after beating fourth-quarter earnings estimates and projecting solid fiscal 2026 growth, with annual revenue surpassing $1 billion for the first time.

Wednesday's Movers to the Downside:

- World's largest spirits maker Diageo fell over 15% after cutting its 2026 sales and profit outlook, citing weaker demand in North America and China, a move that also put downward pressure on Boston Beer, Constellation Brands and Molson Coors.

- GoDaddy slipped 14% despite topping fourth-quarter earnings estimates, as softer 2026 revenue guidance and a bookings miss weighed on sentiment.

- Oddity Tech plunged nearly 50% even though it beat quarterly expectations, warning that algorithm changes at its largest advertising partner could drive a roughly 30% year over year revenue decline in the first quarter.

- First Solar dropped over 13% following weak fourth-quarter earnings and downside revenue guidance for fiscal 2026.

- Card-issuing platform Marqeta declined over 7% as its full-year revenue growth outlook disappointed investors, overshadowing a breakeven quarterly earnings result.

Thursday's Markets and News:

Investors were underwhelmed by Nvidia's earnings report. The "Nvidia Hangover" arrived early. Despite the record numbers, skepticism took hold regarding the sustainability of the AI capex cycle, leading to the largest single-day drop for NVDA since April 2025.

Simultaneously, cracks in the Private Credit market deepened; Blue Owl Capital (OWL) hit a 52-week low as redemption anxieties spread to other major asset managers like Blackstone and Apollo.and considering the stock accounts for about 7% of the S&P 500, it's no wonder that the index sank hard. Tech woes dragged the Nasdaq lower as well, but the Dow, with its many HALO companies, managed to scratch out a win.

Lithium prices remain elevated after Zimbabwe, the fourth-largest producer of the critical mineral in the world, suspended exports in a bid to buoy domestic processing.

Gold fell and oil rose as US and Iranian negotiators met in Geneva to discuss a nuclear deal.

Of further interest:

- The global memory chip shortage could shrink the smartphone market by 13%.

- Retail traders spent this morning buying Nvidia stock in record numbers.

- Unlikely bedfellows: Big Oil is asking President Trump to stop attacking offshore wind.

- Walmart is paying $100 million to settle an FTC lawsuit over deceiving delivery drivers about how much they could earn.

Thursday's Movers to the Upside:

- Stellantis rose over 4% as investors looked past a $26 billion EV-related charge and focused on stronger second-half results that hint at a turnaround.

- eBay popped 3% as the company announced plans to cut 800 jobs, about 6% of its full-time workforce.

- Krispy Kreme gained nearly 30% after delivering its strongest quarterly profit beat in years and issuing a strong sales growth outlook.

- Celsius climbed nearly 7% on fourth-quarter results that topped revenue and earnings expectations, with sales more than doubling year over year.

- Penn Entertainment advanced 16.75% following fourth-quarter revenue and earnings that exceeded Wall Street forecasts.

- Netflix recovered over 13% after announcing that the company is exiting the bidding war for Warner Bros.

Thursday's Movers to the Downside:

- Nvidia fell nearly 5.5% as its latest outlook did little to ease concerns around an AI bubble.

- Broadcom slipped over 3% despite projecting at least 1 million chip sales by 2027—the fruits of its stacked design technology.

- Trade Desk dropped nearly 5% after forecasting Q1 revenue below analyst expectations.

- C3.ai sank 18.5% on a third-quarter miss and newly announced layoffs.

- Synopsys declined 5% after a softer-than-expected full-year guidance overshadowed a 65% revenue surge.

- Egg and butter producer Vital Farms slid over 10% after a weak full-year outlook dampened otherwise solid quarterly results.

Friday's Markets and News:

The "Citrini selloff" reared its ugly head once again as tech stocks tumbled, led lower by software companies at risk of being disrupted by AI.

Oil climbed higher thanks to rising tensions in the Middle East. US and Iranian negotiators failed to secure a nuclear deal, and while talks will continue next week, the US has asked non-emergency staff in Israel to leave the country. Meanwhile, Pakistan has declared "open war" with Afghanistan's Taliban regime.

Gold closed in on one-month highs as investors sought safety after a hotter-than-expected PPI reading sparked stagflation fears. A strong February helped the hot commodity wrap up its seventh straight month of gains.

A "Red Friday" took hold as the Producer Price Index (PPI) came in much hotter than expected (+0.8% core), resetting Fed rate-cut expectations. While markets looked for a soft PCE print later in the quarter, the "Upstream" inflation in PPI rattled investors. The Dow plummeted over 700 points by midday, and the Nasdaq hit its weakest monthly close since March 2025.

Friday's Movers to the Upside:

- Dell rose nearly 22% after posting strong fourth-quarter results, raising guidance, and projecting its AI server revenue will double by 2027 despite industry memory shortages.

- Netflix declined to raise its bid for Warner Bros. Discovery to match Paramount Skydance's new offer. Netflix rose nearly 14%, while Paramount jumped over 20% on the news. Warner Bros. Discovery, however, sank over 2% now that the takeover drama is done.

- AES rallied 6.34% following reports it is in advanced takeover talks with Global Infrastructure Partners and EQT.

- The world's largest dental product maker Dentsply Sirona climbed 15.5% after fourth-quarter revenue beat analyst expectations.

Friday's Movers to the Downside:

- CoreWeave fell 18.51% after issuing first-quarter revenue guidance below Wall Street estimates.

- Sunrun dropped 35% despite beating earnings, as a weak 2026 outlook and a downgrade from Jefferies weighed on shares.

- Rocket Lab slid nearly 5% after delaying the first launch of its Neutron rocket to Q4 2026 due to a testing failure, overshadowing better-than-expected quarterly results.

- Barclays fell nearly 4%, Apollo Global Management dropped nearly 9%, Jefferies Financial Group declined 9%, and Wells Fargo slipped nearly 6% amid concerns over potential exposure to the collapse of UK mortgage provider Market Financial Solutions.

- Zscaler fell over 12% despite beating earnings and revenue estimates, as investors remain uncertain how to value software stocks.

- Quantum computing company IonQ dropped over 6%, reversing part of yesterday's 22% surge.

- Airline stocks sank as geopolitical tensions and rising oil prices rattled the industry. United Airlines fell 8.7%, American Airlines dropped 6.24%, Delta Air Lines slid 6.82%, and Southwest Airlines declined 3.28%.

Notable Earnings to be announced March 2nd–6th:

The actual date may vary, so do confirm with your broker to confirm. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

With the "Nvidia primary" now in the rearview mirror, the market's focus shifts from the AI hardware giants to the software layer and the health of the American consumer. This coming week is a heavy "Retail & Cloud" gauntlet, which will provide the first real corporate commentary on how the "Plan B" tariff pivot is impacting forward guidance for 2026.

Monday: MDB / ASTS / CRDO / AMRC / ASAN / PLUG / RIOT

Tuesday: TGT / CRWD / BBY / AZO / ROST / SE / ONON / GTLB / BOX

Wednesday: AVGO / OKTA / ANF / WIX / AEO / GO

Thursday: COST / MRVL / GAP / KR / BJ / BURL / CIEN / DOCU

Economic Calendar for Week of March 2nd–6th:

Following a week dominated by the "Nvidia Primary" and the administration's pivot to Section 122 tariffs, the focus now shifts back to the structural health of the U.S. economy. This week serves as a critical "Labor Gauntlet," providing the Federal Reserve with the final data points needed to decide if a March rate cut is viable or if sticky inflationary pressures in the service sector will force a continued "Hawkish Pause."

The daily schedule of notable economic data releases is:

Monday: ISM Manufacturing PMI (Feb): A leading indicator of industrial health. After months of contraction, investors are looking for a move toward the 50.0 expansion threshold. Any surge in the "Prices Paid" sub-index will be viewed as an early warning of tariff-induced inflation.

Tuesday: JOLTS Job Openings (Jan): Measures labor market "tightness." A significant drop below 7 million openings would signal that higher-for-longer rates are finally cooling the demand for workers, potentially easing wage-push inflation.

Wednesday: ISM Services PMI: The private-sector precursor to Friday's official jobs report. While often volatile, it provides the first look at whether the "Shadow Banking" liquidity scare is impacting small-business hiring.

Friday:

- Non-Farm Payrolls (Jobs report): Following January's surprisingly robust 130k print, a moderation toward 60k-70k is expected. The "Average Hourly Earnings" data will be the most scrutinized figure; if wages remain sticky above 3.7% YoY, the hope for a March rate cut may officially evaporate.

- Unemployment Rate: Considered one of the most critical "health monitors" for the economy and often referred to as the Federal Reserve's "North Star”. The Fed has a "dual mandate": Keep prices stable (inflation at 2%) and maintain maximum employment.

Closing Thoughts

The "Claude-pocalypse" and the Rise of the Agent Economy

While the Dow's flirtation with 50,000 grabbed the headlines, the most profound shift this week happened in silence—inside the codebases of the world's largest companies.

On February 23rd, Anthropic released Claude Code Security. Within hours, billions in market cap evaporated from "Legacy" cybersecurity firms like CrowdStrike and Palo Alto Networks. Why? Because Claude didn't just scan for bugs; it "reasoned" through 500+ vulnerabilities that had survived decades of human audits. It signaled a transition from Cybersecurity as a Product (something you buy to protect your perimeter) to Cybersecurity as a Utility (something built-in at the point of creation).

From "Know Your Customer" to "Know Your Agent" technology is entering the era of the Digital Asset Agent. Looking towards March, the "out of the ordinary" trend isn't just Bitcoin's price; it's the emergence of autonomous AI agents with their own crypto-wallets. In 2026, technology is moving from AI that talks to AI that transacts. By year-end, "Know Your Agent" (KYA) protocols will be as standard as KYC. This is driving a renewed "Verticalization" of digital assets. It won't be about just trading tokens; liquidity pools will be funded that AI agents will use to settle cross-border micro-payments in milliseconds.

While the headlines focus on physical borders, the real wealth appears to be migrating to decentralized, agent-led networks that don't recognize borders at all. The Anthropic move is potentially a wake-up call. The future belongs to the Orchestrators—the humans who can direct teams of specialized agents to solve architecture-level problems.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.