50,000pt Hangover

February 23, 2026

Market Roundup for the Week

The euphoria surrounding the Dow 50,000 milestone met the cold reality of February as the market navigated a high-stakes "double feature" of legal drama and macroeconomic friction. While the week was defined by intense uncertainty over trade policy, a massive late-Friday "short squeeze" salvaged a green finish for the major indices, saving the S&P 500 and Nasdaq from a deeper retracement.

The primary catalyst for this reversal was a historic constitutional check on executive power. On Friday, February 20th, the US Supreme Court (SCOTUS) struck down the administration's sweeping "Liberation Day" tariffs in a 6-3 ruling. The Court held that the International Emergency Economic Powers Act (IEEPA) does not grant the President unilateral authority to "tax" imports under the guise of "regulating" them. The decision effectively shields the economy from an estimated $1.4 trillion tax burden over the next decade. The markets instantly rallied in relief led by import-heavy retailers and tech giants. However, the US administration immediately pivoted toward alternative statutes suggesting that trade-related volatility has merely entered a new phase of "Plan B" litigation... a 10% global tariff using alternative executive powers.

Macroeconomic data further complicated the narrative throughout the week. Q4 GDP arrived at a lackluster 1.4% annualized rate, well below the 2.5% consensus. Analysts largely attributed this slump to the residual drag of last fall's 43-day government shutdown, which is estimated to have shaved 1.5% off the headline growth figure. However, the labor market remained a bastion of strength, with Initial Jobless Claims falling to 206k. This "K-shaped" divergence—softening growth paired with a tight labor market—kept the Federal Reserve in a "Hawkish Pause," (as Wednesday's FOMC minutes confirmed), a reluctance to cut rates while core PCE remained "sticky" at 3.0%.

The week concluded with a defensive-to-offensive rotation. Investors largely ignored the morning's hotter-than-expected inflation data to focus on the SCOTUS-driven margin expansion for multinationals. As the markets now turn their attention toward Nvidia's earnings next week, the prevailing sentiment is one of cautious optimism, tempered by the fiscal reality of potential multibillion-dollar tariff refunds and the resulting pressure on U.S. Treasury issuance.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

With the VIX climbing back above 20, the "fear gauge" is providing rich premiums.

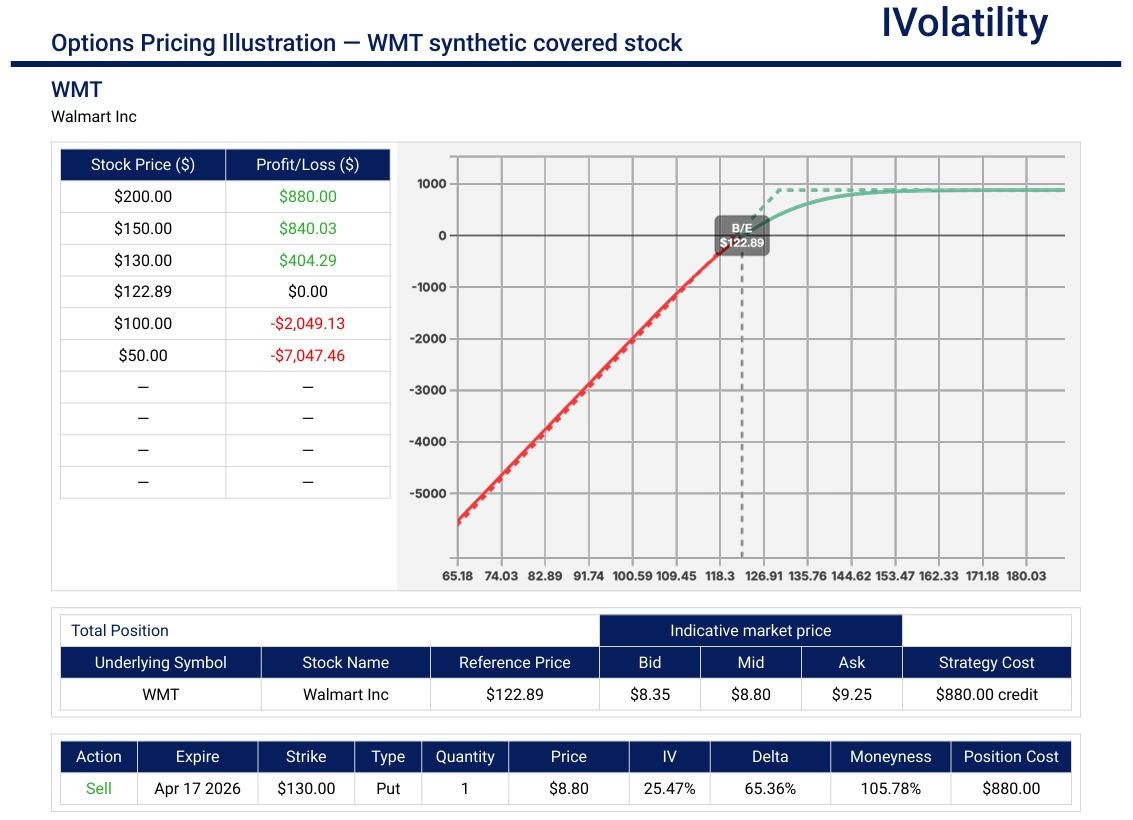

- WMT (Closed at 122.99 on Friday, Feb 20th)

The company reported a blowout earnings quarter on Feb 19, proving to be the "safe haven" of choice. Management announced a new $30 billion share repurchase program and global eCommerce growth of 24%.

- Strategy: Synthetic Covered Stock

- Trade: Sell the Apr17 130put for about $880/contract

(selling the 70delta ITM put is equivalent to buying the stock and selling the 30delta call. The synthetic version holds up a lot less buying power)

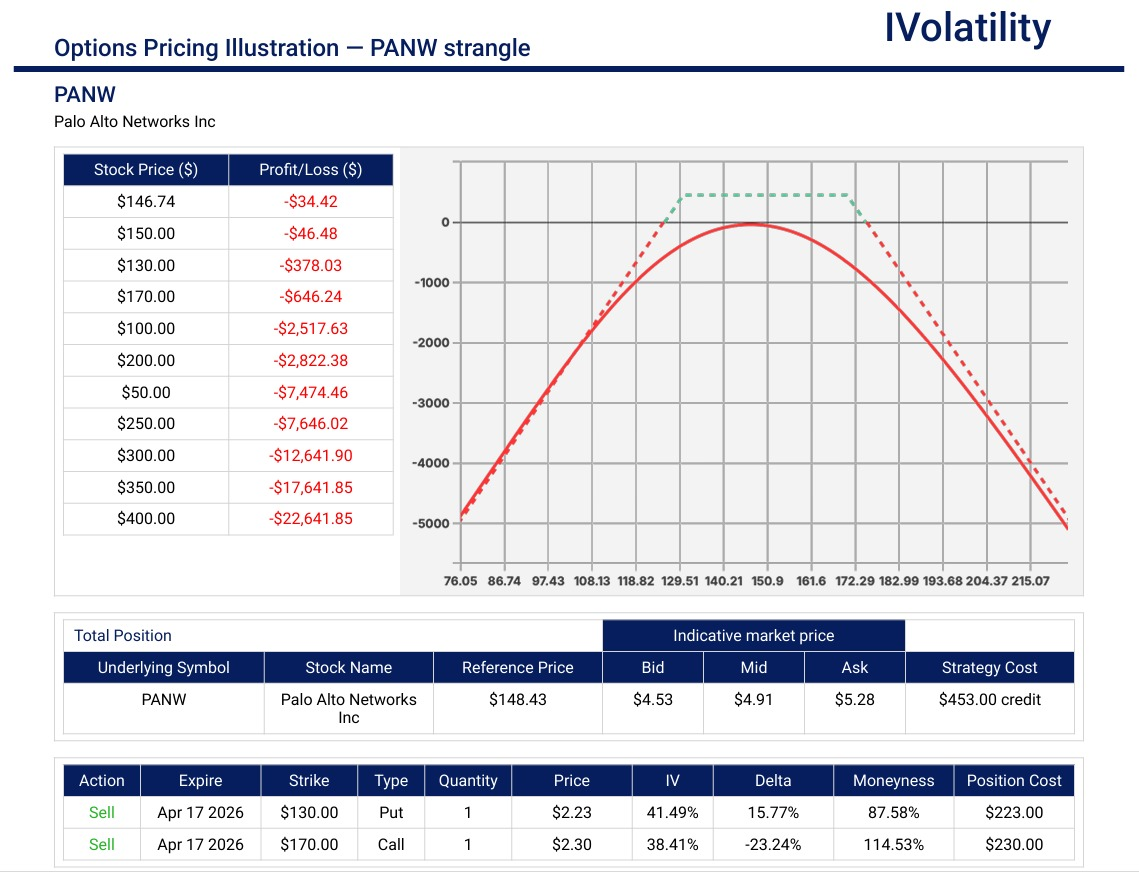

PnL Calculator from the IVolLive Web - PANW (Closed at 148.72 on Friday, Feb 20th)

Palo Alto Networks beat EPS estimates on Feb 17, yet the stock dipped nearly 7% earlier in the week due to weak profit guidance. It has since stabilized, creating a prime "volatility crush" setup.

- Strategy: neutral strangle

- Trade: Sell the Apr17 130/170 strangle for about $520/contract

- Prob of profit: 72%

PnL Calculator from the IVolLive Web

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

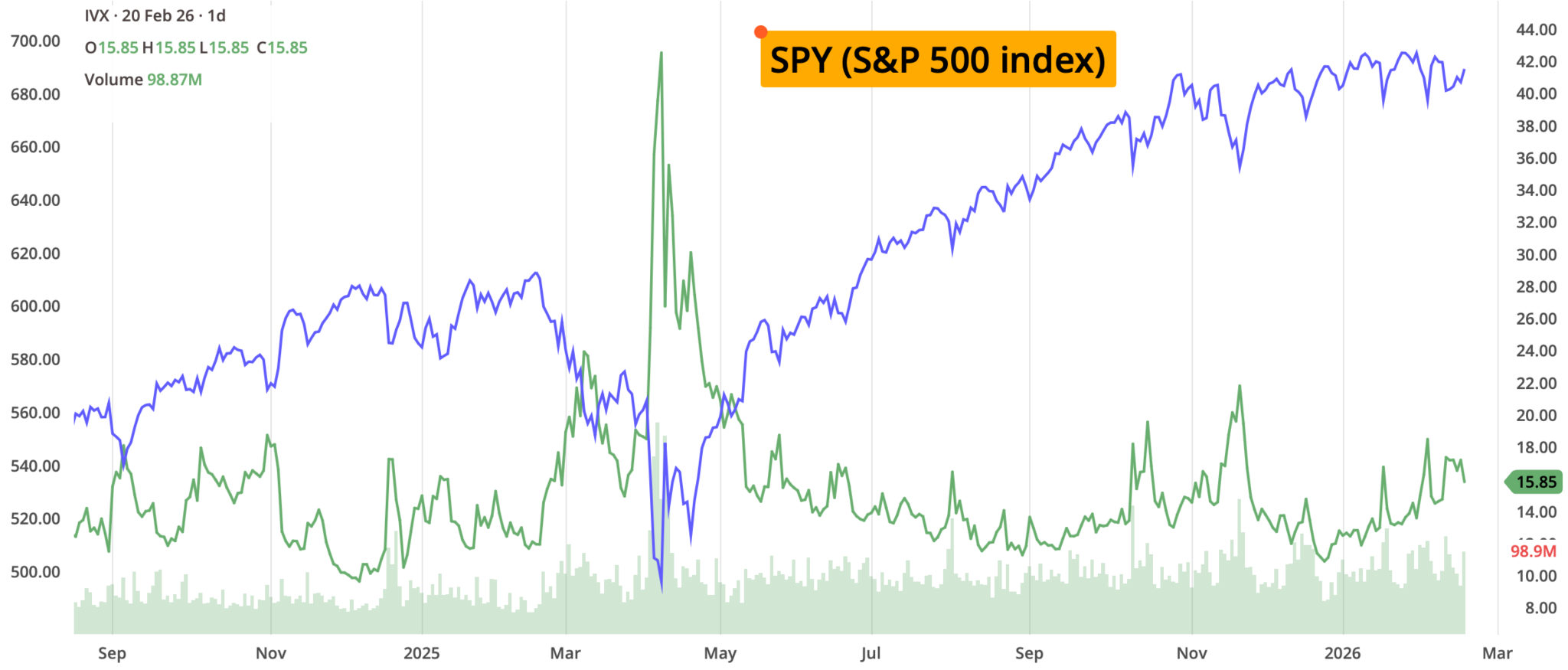

| SPY | 1.13% | |

| QQQ | 1.14% | |

| IWM | 0.63% | |

| DIA | 0.16% | |

| GLD | 1.30% | |

| BTC/USD | -1.18% | |

| TLT | 0.99% | |

| Crude Oil | 5.80% | |

| VIX | -7.42% |

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | 1.34% | |

| FINANCIALS (XL) | 0.73% | |

| INDUSTRIALS (XLI) | 0.64% | |

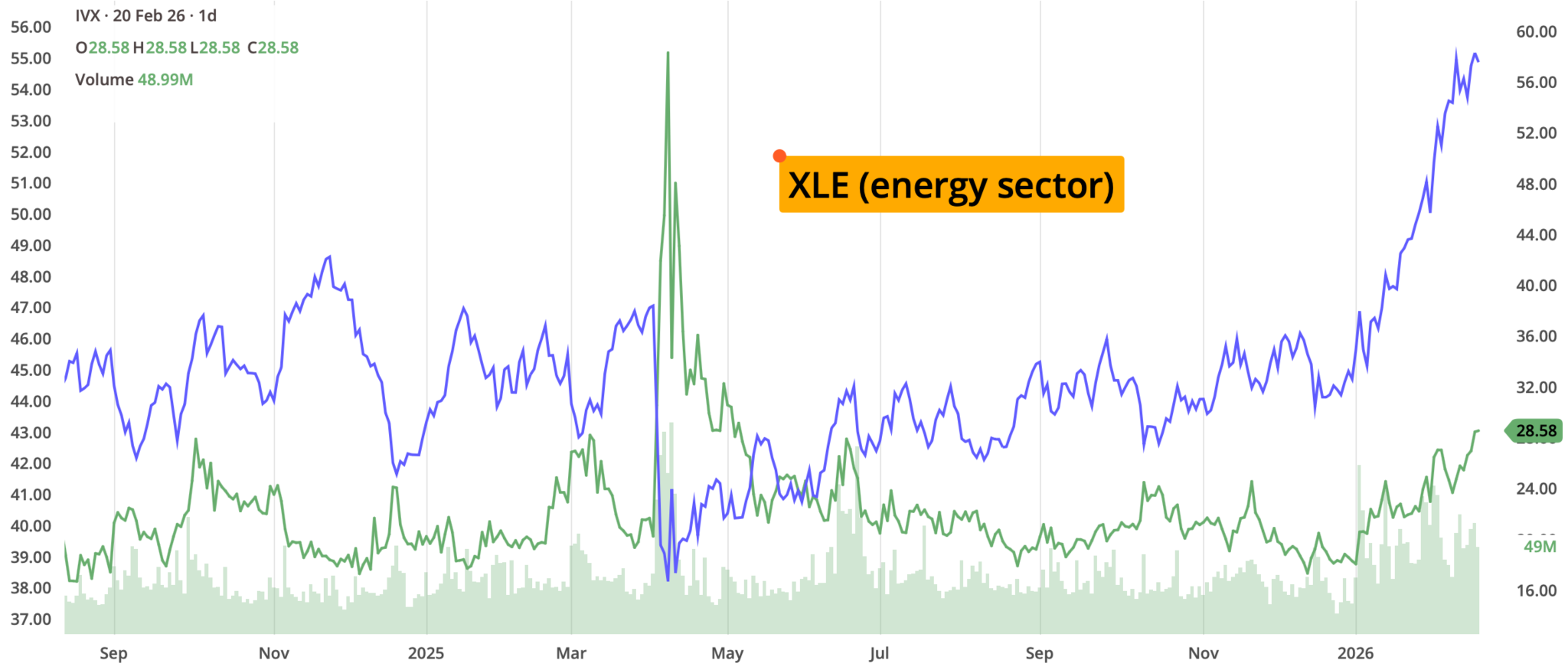

| ENERGY XLE | 1.84% | |

| HEALTHCARE (XLV) | 0.03% | |

| UTILITIES (XLU) | -1.68% | |

| MATERIALS (XLB) | 0.49% | |

| REAL ESTATE (XLRE) | -1.1% | |

| CONSUMER STAPLES (XLP) | -0.25% | |

| CONSUMER DISCRETIONARY (XLY) | 1.27% |

Energy (XLE), the undisputed winner for the week as it captured the geopolitical risk premium from the Iran tensions.

Tech (XLK) & Discretionary (XLY) both saw a significant Friday afternoon boost from the SCOTUS tariff ruling, as traders priced in lower supply chain costs.

The "Defensive Slide" came from the Utilities and Real Estate with significant lags. This might confirm the narrative that as "Risk-On" sentiment returned Friday, capital rotated out of high-yield defensive sectors and into growth.

Healthcare (XLV) finished virtually flat largely held back by the 25% drop in Molina Healthcare (MOH).

Growth in the DIA lagged growth in the QQQ and this could be a signal that growth investors are looking past the GDP miss to focus on the SCOTUS-driven margin expansion for Big Tech.

Despite a 5.80% surge in Crude Oil and geopolitical tension in Iran, the VIX dropped 7.42%. This suggests the market has largely priced in the "Decision Window" and is more focused on domestic policy relief.

Notable gainers for the week of February 16th–20th:

The week was a story of "Retail Resilience" and a dramatic Friday afternoon reversal. While the market spent much of the week in a defensive crouch, the SCOTUS ruling against IEEPA tariffs on Friday sparked a massive "relief rally" across the board.

Walmart (WMT): The undisputed heavyweight of the week. Shares surged to record highs after reporting a Q4 earnings beat and announcing a massive $30 billion share repurchase program. Their 24% global eCommerce growth might prove that they are winning the "AI logistics" war.

Lumen Technologies (LUMN): Continued its 2026 tear, gaining over 12% this week as the "fiber-for-AI" narrative remains the hottest play in infrastructure.

Exxon Mobil & Chevron (XOM & CVX): Both giants gained significant ground as Crude Oil climbed toward $85/bbl on news of the 10-day decision window regarding Iran.

Applied Digital (APLD) & CoreWeave (CRWV): These AI infrastructure plays saw a mid-week rotation back into their shares as investors looked for "tangible AI" bets ahead of the Nvidia earnings.

Notable losers for the week of February 16th–20th:

The "Software Slump" that defined early February refused to break, and a new "Liquidity Scare" in the private credit markets added fresh pressure to the financial sector.

Blue Owl Capital (OWL): The week's biggest headline loser in the financials. Shares tumbled over 6% after the firm restricted redemptions on its retail-focused fund (OBDC II) and shifted to "return of capital distributions." This sparked a broader "shadow banking" sell-off.

Blackstone (BX) & Apollo (APO): Both alternative asset managers dropped more than 5% in sympathy with Blue Owl, as investors reassessed the liquidity and transparency of private credit portfolios.

Palo Alto Networks (PANW): Despite a massive EPS, the stock dropped over 5% as management's conservative 2027 guidance spooked a market that is currently punishing anything less than "perfect" outlooks in software.

Unity Software (U): Slumped 26% following a disappointing earnings report and a sharp downgrade in its growth forecast, becoming the latest victim of the AI-disruption narrative in software.

Peloton (PTON): Continued its downward spiral, dropping another 25% this week after a leadership shakeup and a missed revenue target for the holiday quarter.

Bitcoin (BTC/USD): Slipped below $68,000, losing over 3% for the week. While Gold held firm as a safe haven, Bitcoin continued to behave like a "high-beta tech stock," falling as the Nasdaq wavered.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

Markets were closed in observance of the Presidents Day holiday in the US. However, international sentiment remained cautious following the weekend reports that Chinese organized crime networks laundered $16.1 billion through crypto last year.

Tuesday's Markets and News:

Equities opened the week under pressure as the "Software Slump" continued. Walmart (WMT) hit a historic $1 trillion market cap following a blowout earnings report, providing a defensive anchor for the Dow. However, Amazon (AMZN) corporate job cuts and a widening "K-shaped" economy report (showing lower-income exhaustion) weighed on sentiment. Palo Alto Networks (PANW) reported a beat on Tuesday evening but fell in after-hours on conservative guidance.

Tuesday's Movers to the Upside:

- WMT up over 3% on earnings.

- LEN (+4.1%) and DHI (+3.8%) jumped on the launch of the federal "Trump Homes" infrastructure initiative.

Tuesday's Movers to the Downside:

- PANW down over 7% on guidance.

- MOH down nearly 5.5% on Medicaid reimbursement concerns.

Wednesday's Markets and News:

A mid-week relief rally was led by Nvidia (NVDA) following a massive chip deal with Meta Platforms (META). However, the gains were capped by FOMC Minutes, which revealed a "Hawkish Pause" stance. Anthropic released new AI legal-automation tools, causing a sharp sell-off in "Legacy SaaS" stocks. Globally, France announced a pivot away from Zoom and Teams to sovereign tech alternatives.

Wednesday's Movers to the Upside:

- NVDA jumped over 2% and META rose nearly 2% on the AI partnership.

- PLTR jumped nearly 2% following an analyst upgrade to "Outperform."

Wednesday's Movers to the Downside:

- SNOW dropped over 4% and CRM dropped over 3% as AI-automation fears hit legacy software seats.

Thursday's Markets and News:

Geopolitical tension dominated as the President set a 10-day window for an Iran nuclear accord, sparking a flight to safety. Crude Oil surged past $66/bbl. In the financial sector, Blue Owl Capital (OWL) shook the market by halting redemptions in its $1.8 billion private credit fund, fueling "shadow banking" contagion fears. Initial Jobless Claims fell to a low of 206k.

A "risk-off" mood took hold as President Trump announced a 10-day window for a diplomatic accord with Iran, stationing two aircraft carriers in the region. Initial Jobless Claims fell to 206k, a 5-week low, reinforcing the Fed's "higher-for-longer" stance. Meanwhile, Blue Owl Capital shook the financial sector by restricting redemptions in its $1.8 billion private credit fund, fueling fears of a liquidity crunch in "shadow banking."

Thursday's Movers to the Upside:

- XOM and CVX both jumped over 2% on rising energy prices.

- DE rose over 6% following a strong "Beat and Raise" quarterly report.

Thursday's Movers to the Downside:

- OWL shed over 5% and BX shed nearly 3.5% on the private credit liquidity scare.

- CENT dropped 9.5% after announcing a pause in its buyback program.

Friday's Markets and News:

Markets opened sharply lower after Q4 GDP arrived at a disappointing 1.4%, and Core PCE (the Fed's favorite inflation gauge) remained "sticky" at 3.0%. Markets were deep in the red until midday, when the Supreme Court (SCOTUS) struck down the IEEPA tariffs in a 6-3 ruling. This "SCOTUS Spark" triggered a massive short squeeze that turned the week green. This sent the Dow into green territory, even as Molina Healthcare (MOH) plummeted 25% on a bleak Medicaid outlook.

Friday's Movers to the Upside:

- GOOGL rose over 4% and AMZN rose over 2% as the "Mag 7" led the tariff-relief rally.

Friday's Movers to the Downside:

- NET shed 8% and CRWD shed over 7% after Anthropic's new security features disrupted the cybersecurity narrative.

- MOH shed over 25% after a devastating Medicaid outlook.

Notable Earnings to be announced Feb 23rd – Feb 27th:

The actual date may vary, so do confirm with your broker to confirm. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

The focus of the earnings cycle shifts in the coming week from retail resilience to the structural durability of the AI infrastructure boom. While dozens of mid-cap reports will provide localized volatility, the market is probably singularly focused in its anticipation of Nvidia's (NVDA) Q4 results on Wednesday, which are widely viewed as the definitive barometer for global semiconductor demand and the broader "AI trade."

Monday: D / DPZ / PUBM

Tuesday: CRM / SNOW / INTU / HD

Wednesday: NVDA / BAIDU / HPQ / LOWS

Thursday: BRK.B / TTD / OKTA / DELL

Friday: Z / BBY

Key Economic Indicators due Feb 23rd – Feb 27th:

Given the 2026 backdrop—especially with the delayed data from last year's shutdown still trickling in—the coming week is actually one of the most important of the quarter. We have the Fed's favorite inflation gauge (PCE) and the "World's Most Important Stock" (Nvidia) on deck.

Capital markets are bracing for a high-velocity week as the "inflation vs. growth" debate enters a critical phase. With the Supreme Court having just upended the tariff landscape, traders will be hypersensitive to any data that hints at the Fed's next move in March.

The primary focus will be Friday's PCE Price Index, the Federal Reserve's preferred inflation metric. After a month of "sticky" regional data and geopolitical oil spikes, the market is desperate to see if core inflation is actually cooling or if the 3.50%–3.75% rate range is here to stay.

Traders might keep an eye on Consumer Confidence to be released on Tuesday. Breaking news: On Sunday morning, the European Central Bank (ECB) expressed "confusion" over the U.S. trade trajectory and hence any weakness in U.S. consumer sentiment could be amplified by global trade jitters.

The daily schedule of notable economic data releases is:

Monday: Richmond Fed "CORE Week" Begins. A gathering of prominent economists that often results in "hawkish" or "dovish" headlines throughout the week.

Tuesday: CB Consumer Confidence. Markets are looking for signs that the American consumer is still resilient despite the recent "Credit Crunch" headlines in the private lending space.

Wednesday: New Home Sales. A key gauge for the housing market's sensitivity to the current 4.22% 10-year yield.

Thursday: Initial Jobless Claims. Following last week's 206k print, any move above 230k would likely fuel "rate cut" euphoria.

Friday: Core PCE Price Index. The week's "Main Event." Expected to show if the 2% target is within reach. We also get the Chicago PMI, a vital snapshot of midwest industrial momentum.

Closing Thoughts

For years, "Private Credit" was the preferred vehicle for sophisticated capital—offering higher yields with supposedly lower volatility than public markets. However, the exit door grew narrow this week. Blue Owl Capital (OWL) shifted redemptions in its retail-focused fund (OBDC II) to "return of capital distributions" funded by asset sales, a move that highlights the inherent liquidity risks in shadow banking. When private loan assets are not "marked to market" daily, a sudden rush for the exits forces a reality check that can be disruptive. This is not merely an isolated event; it represents a transparency challenge for the entire $1.8 trillion private credit ecosystem. If the AI bubble defined January, the "Credit Crunch" in semi-liquid funds may be the dominant narrative for the remainder of Q1.

Simultaneously, the market witnessed a historic constitutional check on executive power. The Supreme Court's 6-3 ruling on Friday to strike down IEEPA-based tariffs provided a significant "relief valve" for equities. By ruling that "regulating" commerce does not grant the President the unilateral power to "tax" it through indefinite tariffs, the Court may have shielded the economy from a massive projected tax hit.

Should investors mistake a legal victory for a shift in policy direction? The administration's immediate signal to pursue alternative executive statutes suggests that while the legal framework of the tariffs may evolve, the protectionist stance probably remains intact. As the market prepares for Nvidia's earnings on Wednesday and the PCE inflation data on Friday, the broader economy remains caught between a slowing GDP (1.4%) and a persistent "higher-for-longer" Federal Reserve. Caution is warranted, particularly regarding liquidity traps in private markets and high-valuation software names.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the News tab on our website.